If you're wondering how much gap insurance really costs, you're not alone. For a real-world answer, we analyzed the comments from top-ranking Reddit thread as of February 2026 for term "gap insurance cost" where actual drivers discuss how much they paid for gap insurance. Based on self-reported costs from real people in that discussion, gap insurance typically costs between about $5 and $15 per month when added to an auto insurance policy, or roughly $60 to $180 per year.

Drivers who purchased gap insurance through a dealership reported paying between $400 and $900 as a one-time fee, often rolled into their loan. These findings reflect reported pricing as of February 2026, based on analysis.

That wide range highlights why where you buy gap insurance matters just as much as whether you buy it at all. The same coverage can cost dramatically more depending on the purchase method.

Below, we break down average gap insurance costs by source, explain why prices vary so much, and show you how to get the best value without overpaying.

Key Takeaways

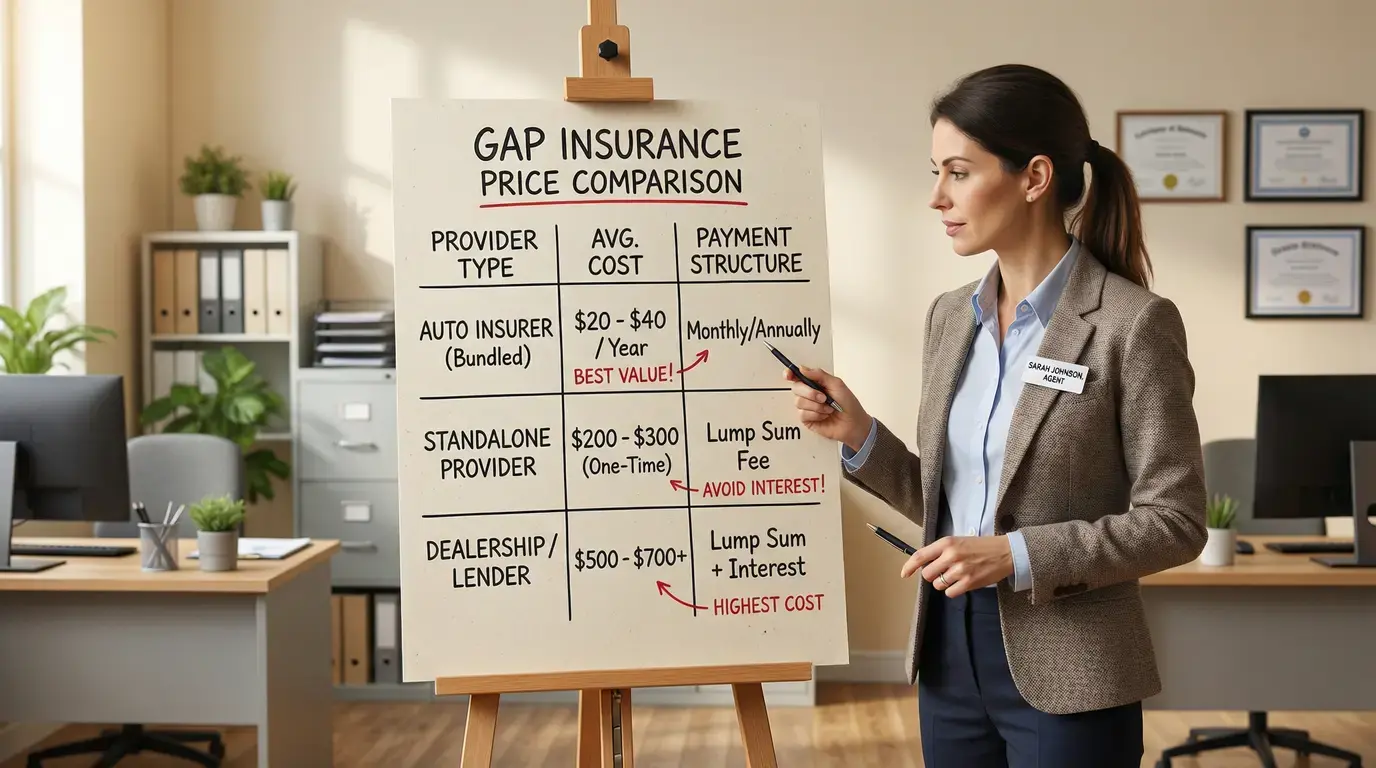

- Gap insurance costs significantly less when purchased through an auto insurer ($20–$100/year) compared to dealerships ($400–$700 one-time fee).

- Dealership Gap insurance, when financed, incurs additional interest charges over the loan term.

- Factors like vehicle depreciation, loan amount, and down payment influence the need and cost of Gap insurance.

- Gap insurance is most beneficial for new cars, leased vehicles, or those with small down payments or long loan terms.

- Always shop around and compare quotes from multiple providers to secure the best price.

- Cancel Gap insurance once you have positive equity in your vehicle to avoid unnecessary costs.

Gap Insurance Cost Comparison by Purchase Method

This table compares the three main ways to purchase gap insurance, showing upfront costs, total cost over a typical 5-year loan, and key advantages of each method. This helps you quickly identify the most cost-effective option for your situation.

| Purchase Method | Upfront Cost | Total Cost (5 Years) | Best For | Key Advantage |

|---|---|---|---|---|

| Through Auto Insurance Company | $0 (added to premium) | $100 – $500 | Most vehicle owners, budget-conscious | Lowest annual cost, easily cancellable |

| Through Car Dealership | $400 – $700 (one-time fee) | $400 – $700+ (plus interest if financed) | Convenience, immediate coverage | Seamless integration into vehicle purchase |

| Through Credit Union/Bank | $200 – $300 (one-time fee) | $200 – $300+ (plus interest if financed) | Existing bank/CU members | More affordable than dealerships |

| Through Standalone Gap Provider | Varies (can be annual or one-time) | Varies | Those needing specific coverage not offered elsewhere | Specialized coverage options |

What Factors Influence Your Gap Insurance Premium?

Several variables determine the specific premium you'll pay for Gap insurance, affecting both the need for coverage and its cost.

- Vehicle Type, Age, and Depreciation Rate: Cars that depreciate quickly, such as luxury vehicles or electric vehicles, often have higher Gap insurance costs due to a larger potential gap between loan balance and ACV (Future Market Insights). New cars lose approximately 20% of their value in the first year alone.

- Loan Amount and Down Payment: A larger loan amount or a smaller down payment increases your risk of negative equity, making Gap insurance more critical and potentially influencing its cost.

- Your Insurance Provider's Pricing Structure: Different insurers have varying rates, with some offering Gap as a low-cost add-on to comprehensive and collision coverage, often around 5–6% of those premiums.

- State Regulations and Requirements: Costs can fluctuate significantly by state; for example, annual costs range from $40 in West Virginia/Iowa to $210 in Montana.

How Do You Calculate the True Cost: One-Time vs. Annual Premiums?

To understand the true cost of Gap insurance, it's essential to compare one-time fees from dealerships and lenders with the annual premiums offered by insurance companies over your typical loan period.

When you purchase Gap insurance through a dealership, the one-time fee of $400–$700 is often financed into your car loan, meaning you pay interest on it for the entire loan term. For a 60-month loan, a $600 dealership fee could effectively cost you more like $700–$800 after interest.

In contrast, an insurance company add-on costing $60 per year would total $300 over a 60-month (5-year) loan, with no interest charges. This illustrates potential savings of hundreds of dollars by choosing an insurer.

When Are Gap Insurance Costs Worth It?

Gap insurance provides significant value in specific financial and vehicle ownership scenarios, protecting you from substantial out-of-pocket expenses.

- High Depreciation Vehicles: If you own a vehicle known for rapid depreciation, such as many luxury cars or electric vehicles, Gap coverage is highly beneficial (Future Market Insights). These vehicles can lose value quickly, creating a large gap between their market value and your loan balance.

- Small Down Payments or Long Loan Terms: When you make a down payment of less than 20% or opt for an extended loan term (e.g., 60 months or more), you're more likely to owe more than your car is worth for a longer period. Gap insurance mitigates this negative equity risk (Edmunds).

- Leased Vehicles: Gap insurance is often required or strongly recommended for leased vehicles (Data Insights Market). Lessees are typically responsible for the full payoff amount if the vehicle is totaled, making Gap essential to cover the difference between the actual cash value and the lease payoff.

You might consider skipping Gap insurance if you made a large down payment (20% or more), have a short loan term, or drive a vehicle that holds its value exceptionally well, as you may quickly reach a point of positive equity.

How to Get the Best Price on Gap Insurance

Securing the most affordable Gap insurance requires proactive comparison shopping and understanding your options.

- Shop and Compare Quotes: Obtain quotes from multiple auto insurance providers, as rates can vary significantly. Insurers typically charge $20–$100 per year, far less than dealership options.

- Ask About Bundling Discounts: Inquire if your current auto insurer offers discounts for bundling Gap coverage with your existing policy. Many insurers include it as a low-cost add-on.

- Decline Dealership Gap Insurance: Always negotiate or decline Gap insurance offered by the dealership. Their prices are often marked up significantly, and you can almost always find a cheaper alternative elsewhere.

- Review and Cancel Annually: Monitor your loan balance and vehicle value. Once your loan balance is less than the car's actual cash value, you no longer need Gap insurance. You can cancel it and potentially receive a prorated refund if you paid upfront (InformedIQ).

Conclusion: Making an Informed Gap Insurance Decision

The cost of Gap insurance is a critical consideration for vehicle owners, particularly those with new cars or leases. While dealerships may offer it as a convenient, albeit expensive, add-on, the most financially prudent approach is typically to purchase it as an economical add-on to your existing auto insurance policy, often for just $20–$100 per year.

By understanding the factors that influence pricing and actively shopping around, you can avoid paying hundreds of dollars more than necessary. Evaluate your individual vehicle, loan situation, and depreciation risk to determine if Gap insurance is a worthwhile investment for your financial protection.

Before finalizing your vehicle purchase or lease, take the time to compare quotes from your current insurer, credit unions, and independent providers. This informed decision-making process will ensure you secure adequate coverage at the best possible price.

Frequently Asked Questions About How Much Does Gap Insurance Cost

Based on AI analysis of real driver reports and national pricing data, gap insurance typically costs between $20 and $100 per year when added to an auto insurance policy. Drivers who purchase gap insurance through a dealership often pay a one-time fee of $400 to $700, and sometimes more if the cost is rolled into a loan with interest.

Dealerships frequently mark up gap insurance because it's sold as part of the vehicle purchase process and financed into the loan. This markup can increase the price by 100–250% compared to insurance-company add-ons, and financing the fee means you also pay interest over the life of the loan.

Gap insurance is almost always cheaper when paid monthly or annually through an auto insurance provider. Monthly costs typically range from $2 to $10, while a one-time dealership payment can cost several hundred dollars upfront and more over time if financed.

The cheapest option is usually adding gap insurance to your existing auto insurance policy, where it's offered as a low-cost add-on. This approach typically costs $20–$100 per year, making it far more affordable than dealership or lender options.

Most drivers only need gap insurance during the first 2–3 years of ownership, when vehicle depreciation is highest and loan balances are still relatively large. Once your loan balance drops below your car's actual cash value, gap insurance is no longer necessary.

Yes. Gap insurance can usually be canceled once you no longer need it. If purchased through an insurer, it can typically be removed at any time with no penalty. If purchased through a dealership, you may be eligible for a prorated refund, although some providers charge processing fees.

Gap insurance is generally worth it if you finance a new vehicle with a small down payment, choose a long loan term, or lease a vehicle. In these situations, depreciation can outpace loan repayment, leaving you exposed to out-of-pocket costs if the vehicle is totaled or stolen.

Yes. Vehicles that depreciate quickly, such as luxury cars, electric vehicles, or high-MSRP models, may carry slightly higher gap insurance costs because the potential difference between loan balance and vehicle value is larger.

Gap insurance is not legally required, but it is often required or strongly recommended for leased vehicles. Lenders may also require it for certain loan structures, especially those with low down payments.

You may not need gap insurance if you made a down payment of 20% or more, chose a short loan term, or own a vehicle that holds its value well. In these cases, you're more likely to reach positive equity quickly.